The Oil Can't Move

Why this crack spread episode breaks the historical pattern, and what that means for prices through summer.

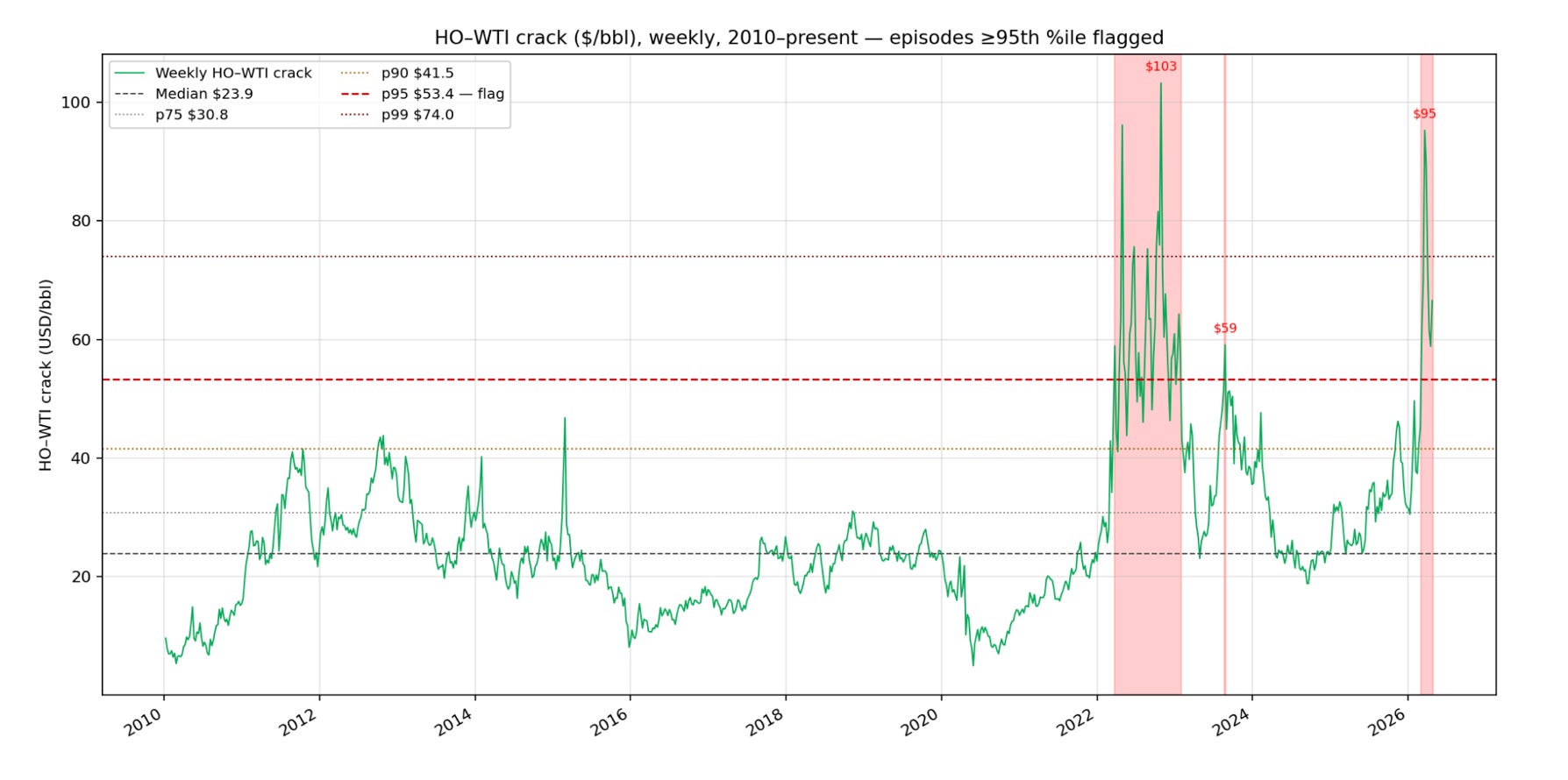

The HO-WTI crack spread is at $67. That’s the 99th percentile of the last 15 years. Only twice since 2010 have we been at these levels: the 2022 Ukraine response and a brief 2023 spike.

In both cases, crude fell over the next 90 days. Inventories rebuilt. The refining industry captured the margin and the crisis resolved through supply response, not through crude continuing to spike.

If history is a guide, the current episode resolves the same way. Cracks compress. Crude eases. Refiner stocks hold their gains. Inventories rebuild.

I think that’s wrong this time, for a specific reason: the supply response that fixed the previous episodes isn’t available.

Hormuz is effectively closed. Russia is embargoed and its refineries are being systematically degraded by Ukrainian strikes. Even if Hormuz opened this afternoon, tankers need 20-40 days to reach Europe and Asia. Middle East refining capacity damaged in the war needs months to years to restart, per Wood Mackenzie. The rearrangement mechanism that worked in 2022, where Russian barrels found non-EU buyers and US barrels filled Europe, doesn’t work when the physical infrastructure is broken instead of rerouted.

The historical pattern assumed the oil could move. This time it can’t.

What the data says

I collect an obscene amount of data on these markets. I went back and looked at what the data says during times of large HO-WTI crack spreads. Going back to 2010, the P95 threshold is $53.36, and only three episodes total have hit this level.

The first episode is the October 2022 Ukraine response. The peak there was $103. It spent 34 weeks above P95. Once it dropped, crude fell 8-12% over those 90 days, and distillate inventories built 10-12 million barrels.

In August 2023, we hit a peak of $59 as a single week spike. Crude fell 5% over the 90 days after that.

In that third instance, the peak has been $95. The current episode is at 8 weeks and counting, with cracks still rising. We may retest the $95 peak before this resolves.

Across the 2 mature episodes, the average outcomes were a 6.6% drop in crude oil prices, a 1.5% increase for the XLE, and an increase of 1.8 MMbbl in distillate inventories.

The historical pattern is clear. Cracks at this level have resolved through crude falling and inventory rebuilding, not through further crude spiking. Refiner equities roughly held their gains even while crude declined, so the margin capture there was real and persistent.

Why The Pattern Worked Before

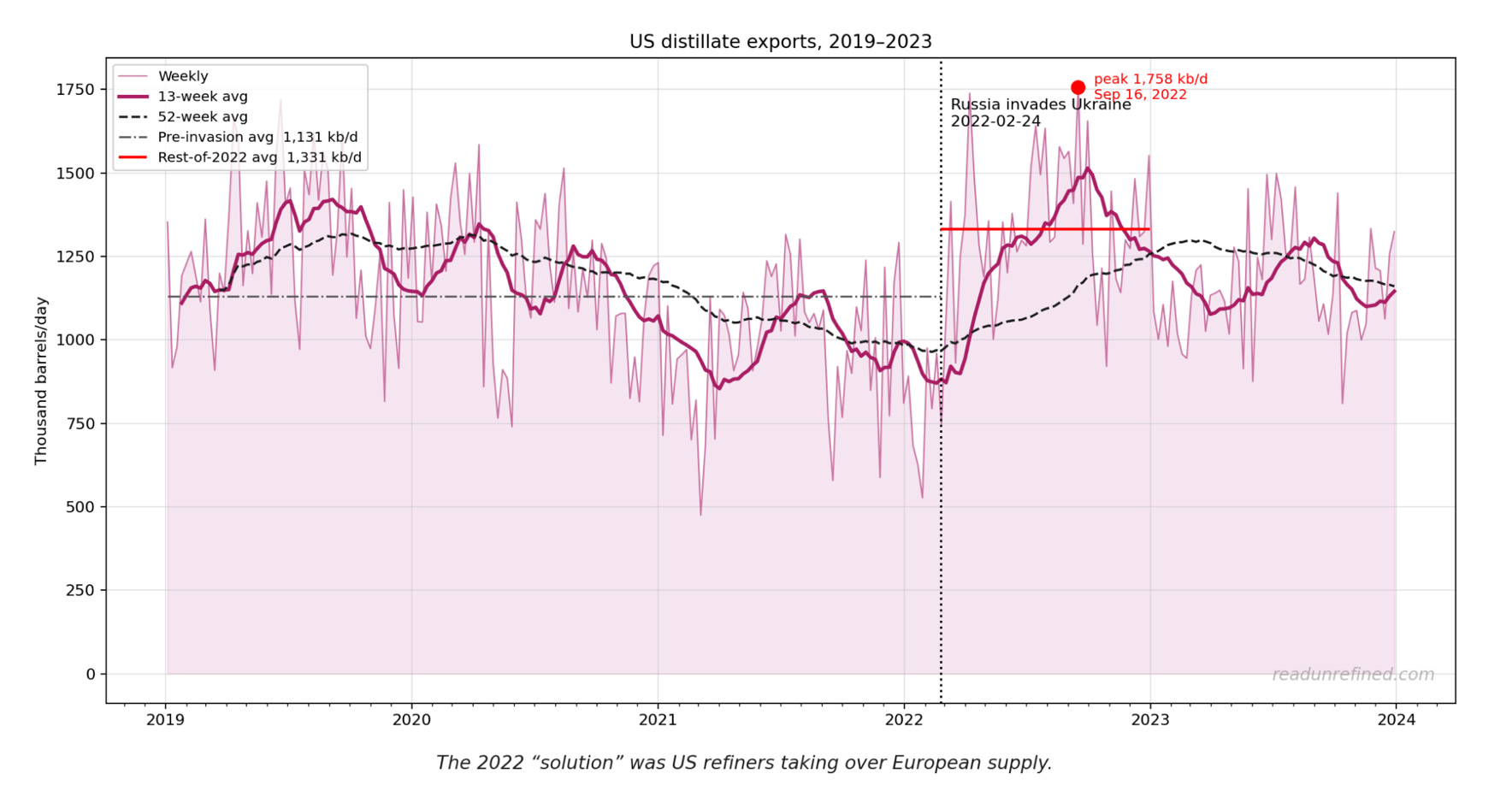

In 2022, the shortage was a sanctions problem, not a physical supply problem. Russian oil did not just disappear, it just moved to new buyers in India, Turkey, and China. They absorbed what Europe stopped buying.

Meanwhile, the US Gulf Coast took over as Europe’s primary diesel supplier, and exports rose from their normal 1 MMbbl/day range to a sustained 1.3 to 1.5 MMbbl/day by late 2022.

That was just a logistical adjustment. It took 30 to 60 days for shipping patterns to rewire, and then the system found its balance. The 2023 spike was even simpler. It was a brief refinery outage. Normal operational recovery, cracks compressed within weeks.

What’s Different This Time?

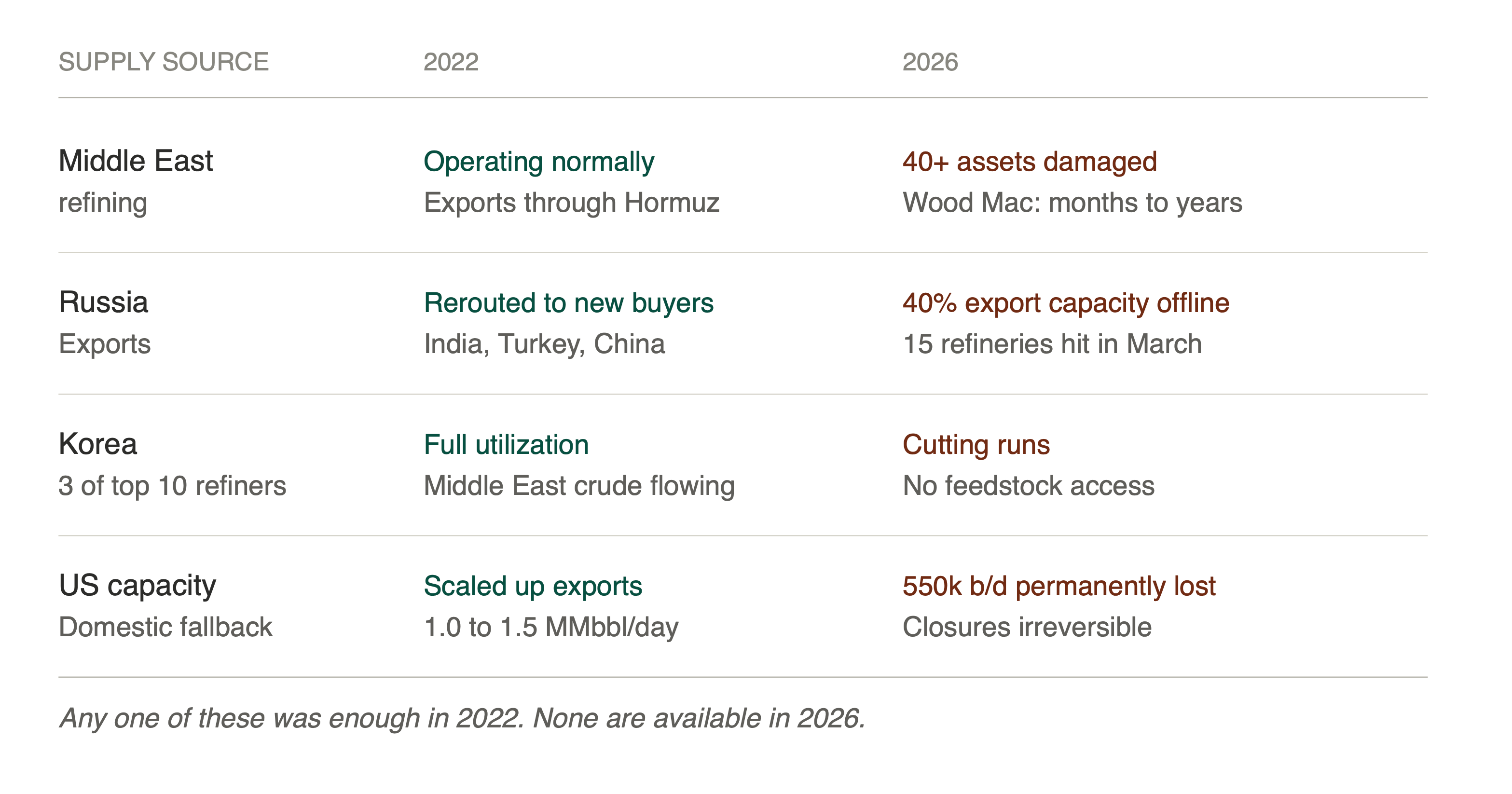

The thing that is different this time is that those past high-crack episodes resolved because supply was available somewhere and the market just needed time to redirect it. You could argue that the supply is there somewhere today, but there is no way to redirect it. It is trapped.

The Middle East refining capacity is physically damaged. Wood Mackenzie says that it will be months to years before most of that can restart. You have at least 40 damaged energy assets across 9 countries. Iraq alone would need 6 to 9 months to get most of its capacity restarted.

This time it is not sanctions. You cannot reroute around a damaged catalytic cracker. The capacity is either online or it is offline. Right now, significant capacity is offline.

Russia faces sanctions, and its refineries are also being actively degraded. Ukraine hit 15 oil refineries in March alone, according to Ukrainian Commander-in-Chief Oleksandr Syrskyi. Tuapse, one of the top 10 Russian refineries, was hit by drone strikes on April 16, knocking out a facility that processes 240,000 barrels a day. According to Reuters calculations, roughly 40% of Russia’s oil export capacity is currently offline due to a combination of Ukrainian strikes, pipeline damage, and tanker seizures.

South Korea has 3 of the top 10 refineries globally, but they are cutting runs because they cannot get Middle East crude through Hormuz. Even if Hormuz opened right now, it would still take 20 to 40 days for those tankers to arrive in Korea.

US capacity is permanently smaller. Facilities including LyondellBasell in Houston, Phillips 66 in Wilmington, and Valero in Benicia account for 550,000 barrels a day that have been removed from US capacity in the last 18 months.

Every supply response mechanism that worked in 2022 is either broken, degraded, or physically destroyed. You cannot rearrange your way out of this with ease.

What that implies for prices

As mentioned throughout, cracks historically compress within 60-90 days of P95 peaks. This time, however, they will likely persist. My target range is that these will remain at $60-$80 through the summer, and they will probably be even wider if policy intervention risk rises.

Crude, as we mentioned as well, also historically falls after peak prices, usually about 6.6% over the subsequent 90 days. This time though, it is probably going to continue grinding higher through the summer. $100 to $120 is a range that crude will absolutely sit in.

But honestly, if this drags on, $200 is on the table. The difference between my base case and the $200 scenario isn’t the mechanism, it’s the timeline. If Middle East refining starts coming back by late summer, we settle in the $100 to $120 range. If it doesn’t, and Ukraine keeps hitting Russian refineries through the fall, there is no ceiling I can defend analytically. Wood Mackenzie has already floated $150 oil if Hormuz stays shut. The market just keeps pricing scarcity until something breaks.

The XLE is usually flat throughout these sorts of events. But this time, refiners in that bucket should contribute a little bit more meaningfully. VLO and MPC are names that I would look to for potential outperformance over the coming months. As we continue to see distillate inventories drop, and Valero and Marathon are both heavy distillate producers, we will see those distillates drop probably down below 100 MMbbl as we continue to draw through May.

Both VLO and MPC report Q1 earnings in the next two weeks, April 30 and May 5 respectively. If the thesis is right, both print blowout numbers and guide strong for Q2. That is the first real test of whether the refining bottleneck story translates into actual captured margin.

What would make me wrong

There are plenty of things that make this not as dire a scenario as I am currently laying out, or as others are currently laying out, so it is worth at least talking them through a little bit.

The first point is that Middle East refining restarts faster than Wood Mac suggests. If 1 to 2 million barrels a day of capacity can come online by the end of June, the physical supply story improves materially, and that could change the outcomes drastically.

A Ukraine-Russia ceasefire that stops Ukraine from hitting some of these Russian refineries does not fix the situation, but it does stop it from getting worse. That is another option we have.

The biggest and most annoying option we have is demand destruction that accelerates faster than inventory draws. We are talking about demand destruction at a scale we haven’t seen outside of COVID. This includes jet fuel demand collapsing to near zero and diesel usage falling significantly. That affects trucking, freight, and shipping, as all these sectors would cut the amount of goods being moved. It would have to be a quick and fast cut, and there is no indication that is starting yet.

Other factors that could be on the list include export restrictions from major producers such as Canada, Brazil, Guyana, and the United States, or a coordinated global SPR release. If all IEA members release simultaneously, it would be unprecedented, but it is not impossible if prices spike materially higher.

The Trade

There are a few trades you could make if you believe this thesis. You could go long on the HO-WTI crack spread, which involves buying heating oil and selling WTI one for one. Heating oil is currently at $67. There is room to reach $80 to $90 if the thesis plays out, and there is room even beyond that.

The easiest trade to hit on is going to be going long on refiner equities like Valero or Marathon Petroleum. VLO is the most distillate heavy of the refiners available in the United States. If exports continue, Valero is going to benefit massively. Marathon is much cheaper on multiples and is still a distillate heavy refiner.

The most obvious short position, if you believe this thesis, is the transportation sector, especially airlines. Lufthansa just announced it is cutting 20,000 flights through October to save on jet fuel, citing the doubling of fuel prices since the Iran war began. KLM, SAS, Aer Lingus, and Norse Atlantic are making similar cuts. The head of the IEA said Europe has “maybe six weeks or so” of jet fuel supplies left. These businesses will have to keep cutting routes and pass fuel surcharges to customers.

A Closer Look at Marathon

Of all the refining equities that you could own to express this thesis, Marathon Petroleum is the one I keep coming back to.

Here is the short version of why Marathon. MPC operates 13 refineries with 3,000,000 barrels per day of crude distillation capacity. The flagship location is the Galveston Bay Refinery in Texas City. It is one of the two largest refineries in the United States and processes 631,000 barrels per day. This single facility is a meaningful chunk of the U.S. Gulf Coast export machine that Europe has been buying from since losing Middle East supply.

The numbers from 2025 demonstrate performance before the current crack environment was in place. MPC delivered $13.22 adjusted EPS for the full year, with Q4 at $4.07 adjusted per share. Refining margins expanded 44% year-over-year to $18.65 per barrel. Refinery utilization averaged 94% for the year with margin capture at 105%. It returned $4.5 billion to shareholders in 2025 through dividends and buybacks. They are executing phenomenally well for a refiner.

That was all before the HO-WTI cracks doubled from $28 to $67. The 2026 setup is materially better than what drove those 2025 numbers, and the company is already printing at nearly full capacity.

MPC normalized EPS is expected to nearly double from $10.70 in 2025 to around $21 in 2026. That number is before anyone seriously prices in the refining bottleneck thesis that is going to play out through the summer. If cracks can stay at $60 through Q2 and Q3, that $21 EPS is probably conservative.

There are a couple of things I wanted to call out that are different for MPC compared to the broader refining group.

At first, they run roughly 50% sour crude across their system, about 10% above their closest peer. That means every $1 widening in the sour differential is worth roughly $500 million in annual earnings. With Venezuelan crude starting to flow back to global markets and Middle East sour supply disrupted, those differentials are moving in MPC’s favor.

In the West Coast, the closure of LyondellBasell, and other facilities means MPC is essentially the primary supplier in Los Angeles and the Pacific Northwest. PADD 5 is where retail diesel has been rising fastest in our data, and MPC is able to capture that directly.

Third, the capital spending is going in the right direction. They are building a 90,000 barrel per day distillate hydrotreater at Galveston Bay to upgrade high sulfur distillate into ultra-low sulfur diesel. This is exactly the right product that is in shortage right now and will still be in shortage for years to come. The project finishes at the end of 2027 with $350 million of spend in 2026 and $225 million in 2027. By the time it comes online, ultra-low sulfur diesel will either still be structurally tight and MPC gets paid, or Middle East refining will have fully recovered and MPC will have the most distillate-capable Gulf Coast asset regardless.

And a fourth, Marathon Petroleum Corporation owns a majority stake in MPLX, their midstream partnership, which distributes cash back to MPC regardless of where refining margins sit. This basically provides a floor under the dividend and capital return program even if cracks compress later in the year. You get refining upside with a midstream backstop.

Marathon is trading at around $220 per share today, up from a 52-week low of $132. Consensus price targets have it going to $244, with Wells Fargo high at $331, pricing to me what the bull case actually looks like if Gulf Coast utilization stays elevated through the summer. A low target of $174 assumes full crack spread normalization back to pre-war levels, which is a scenario I am clearly arguing against in this piece.

Overall, if I had to pick one refiner to own as a single name bet on this thesis, it would be MPC. Valero is cleaner on the distillate purity and is the obvious choice on the thematic fit, but Marathon has better multiple support, cleaner operating momentum, and the MPLX floor. For a piece arguing that this crack environment persists longer than history suggests, you want a name that is already executing well.

We will be back on May 6, which is one day after Marathon reports their earnings. We will be back to discuss those and see if the thesis is holding up early in the game.

Closing

The pattern history shows is not irrelevant, it is informative. However, it relied on a specific precondition: oil that could move. That precondition is not present this time. We have specific damage to physical infrastructure, active degradation of alternative suppliers, and broken shipping routes. History says this resolves in 60 to 90 days through a supply response. I am saying a supply response cannot happen. This resolves through demand destruction or policy intervention instead. Those have different timelines, different price paths, and no historical playbook.

The oil can’t move. That’s the whole story.